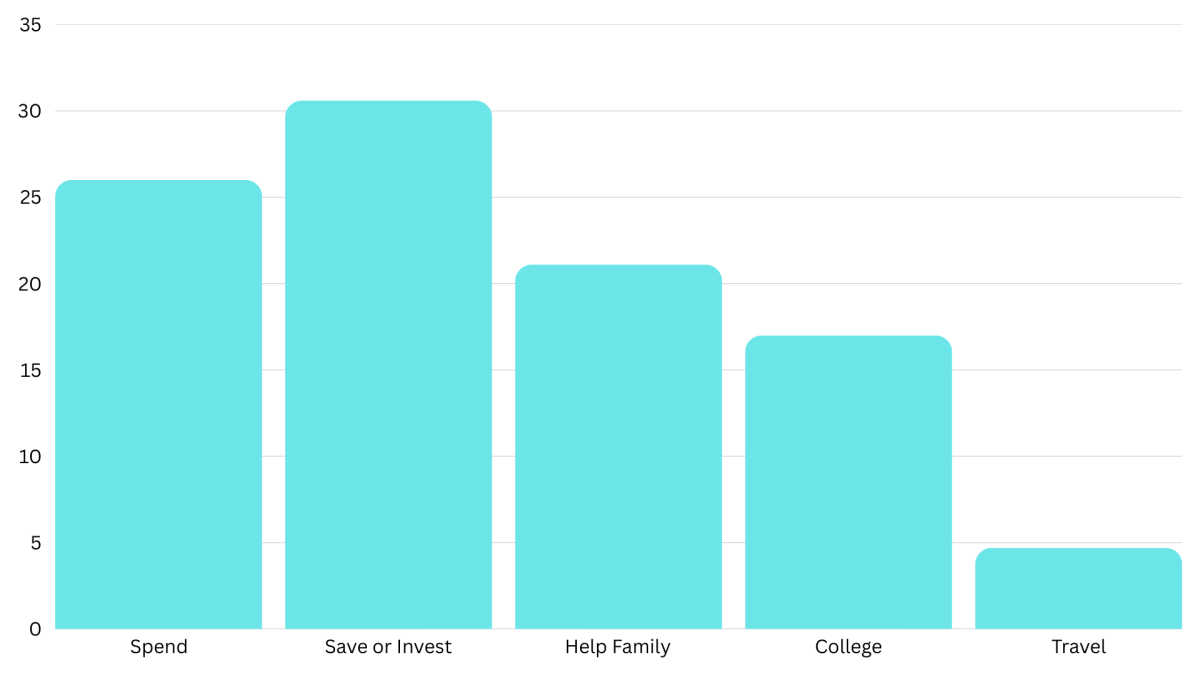

Everyone jokes about winning a million dollars, but what would a student actually do with such a huge amount of money? According to a recent Fielder poll, about 30% of students said they would save or invest the money, but the other 70% had various other plans.

Khole Fuller, sophomore, said the first thing she is buying is a house, then she’d “invest most of the money so it can grow.” She’d definitely spend some on “a bunch of dogs, as many as I can,” along with a big backyard for them. Fuller said having a million dollars would help her feel stable and make life easier on her and her parents.

Javier Gracia Delach, freshman, would plan to be the most organized.

“I will send a lawyer or someone I trust to go get the money so people don’t ask me to borrow money,” Delach said. He also gave a clear description of what he would do with his money.

“I’d invest about 60% of it into the stock market, so it grows over time, donate 20% to charity, and give 10% to my parents and keep 10% as a rainy day fund,” Delach said. He said he isn’t a big spender, but he might buy a car. He feels the money would mostly help him get through school debt-free.

Jacob Maltius, senior, said he wouldn’t buy anything at first and would save everything through college.

“Having a million dollars would make my financial life a lot easier with no debts coming out of college. It basically sets me up for the future,” Maltius said.

If he were older, he would put around 70% into an index fund so it can grow over the years. He said he would help his family and would probably buy a car once everything is set.

Teachers also would have plans if they were to win big money. Jim Kappas, economics teacher, said a lot of people lose such big winnings so fast because they can’t stay disciplined.

“Avoid becoming instantly complacent or changing your long-term, disciplined approach,” Kappas said. “In other words, don’t switch up your whole life just because you suddenly have money.” He also warned that people usually get in trouble by spending too fast or hanging around people who take advantage of them.

“Make your money work through Investments, pay your expenses, and have an emergency fund; everything else should be invested,” Kappas said. “You could be making $100,000 in interest just having your money in a proper investment.”

Arleth Chavez, junior, landed in the 30% of people who would rather invest it than spend it. She said she wouldn’t buy anything right away because she’d help both her family and her friends as well, and the main thing she would buy when she is ready is a house.

“It would probably help me pay for the house for my parents and pay for college,” Chavez said.

In the end, every student had their own idea of what being a millionaire will look like: dogs, houses, savings, college, charity, travel. Even though no one is getting a million dollars anytime soon, the answer showed what they value most: their families, their futures, and maybe a couple of dreams purchased along the way.